The Basics

Imagine handing someone your wallet and saying: “Use this to take care of my kid. Pay for their school, their rent, their doctor. But don’t spend any of it on yourself.”

That’s a trust, stripped down to its core. One person gives money (or property) to another person, with a set of rules about who it’s supposed to help and how.

But a trust isn’t a bank account. You can’t just walk up to an ATM. A trust is a set of rules written into a legal document. Those rules say: who gets what, when they get it, how much they can receive, and under what conditions. The rules are binding. They’re not suggestions.

There are three roles in every trust:

and puts money in

according to the rules

money is supposed to help

The trustee is legally obligated to follow the rules and act in the beneficiary’s interest — not their own. This obligation has a name: fiduciary duty. It is the highest legal standard of care one person can owe another. It means: your job is to take care of this person, period.

Think of it this way: the settlor writes the instructions. The trustee follows them. The beneficiary receives the benefit. When those roles stay separate and the trustee does their job honestly, the system works. When they don’t, things go wrong fast.

Why Do Trusts Exist?

Trusts exist because sometimes people need protection — either from the world or from themselves. Here are the most common reasons someone creates one:

To protect people who can’t manage money themselves

Children, elderly family members, or individuals with disabilities may not be able to handle large sums of money on their own. A trust puts a responsible person in charge so the money is used properly.

To keep money in a family across generations

Grandparents might want their savings to help not just their children, but their grandchildren too. A trust can hold assets for decades and distribute them according to rules that outlive the person who created it.

To protect assets from creditors, lawsuits, or government agencies

Money inside certain trusts is harder for outside parties to reach. For someone with disabilities, this is critical — assets held in the right kind of trust won’t disqualify them from receiving government benefits like Medicaid or SSI.

To make sure money is used for specific purposes

A trust can say: this money is for education. Or housing. Or medical care. The trustee can’t redirect it to other things. The rules are the rules.

Common examples: parents setting up a trust for a child with disabilities so government benefits aren’t disrupted. Grandparents leaving money specifically for college tuition. A spouse ensuring their partner is cared for after they die. These aren’t exotic financial instruments — they’re tools families use to protect people they love.

What a Trustee Is Supposed to Do

If you take one thing from this page, let it be this: a trustee’s job is to serve the beneficiary, not themselves. Full stop. No exceptions.

The legal term for this obligation is fiduciary duty — the highest standard of care recognized in law. Here’s what it requires:

Act in the beneficiary’s best interest — always

Every decision the trustee makes must prioritize the beneficiary. Not the trustee’s convenience, not the trustee’s finances, not the trustee’s preferences. The beneficiary comes first.

Keep accurate records and provide accountings

A trustee must track every dollar that comes in and goes out, and in most states, they are legally required to provide an accounting when the beneficiary asks for one. If a trustee refuses to show you where the money went, that is a problem.

Never use trust money for their own benefit

The trust money isn’t the trustee’s money. They can’t borrow from it, invest it for their own gain, or use it to cover their personal expenses. The money belongs to the beneficiary — the trustee is just the person who writes the checks.

Avoid conflicts of interest

A trustee must not put themselves in a position where their personal interests conflict with the beneficiary’s interests. If a trustee stands to gain — or to lose — from a decision they make about your money, that is a conflict.

Think of it like a babysitter. You trust them to take care of your child. You don’t expect them to raid your fridge, invite friends over, or decide your kid doesn’t need dinner because it’s inconvenient. A trustee who violates these duties can be sued, removed, and held personally liable for damages. Fiduciary duty isn’t a guideline — it’s a legal standard with teeth.

Key Terms, Explained Simply

-

Settlor / GrantorThe person who creates the trust and puts money into it. They write the rules. Sometimes called the “grantor” or “trustor” depending on the state.

-

TrusteeThe person who manages the trust money according to the rules. They have a legal duty to act in the beneficiary’s interest, not their own.

-

BeneficiaryThe person the trust money is supposed to help. They’re the whole reason the trust exists.

-

Fiduciary DutyThe legal requirement to act in someone else’s interest, not your own. It’s the highest standard of care one person can owe another under the law.

-

Sole DiscretionWhen a trust gives the trustee “sole discretion,” the trustee gets to decide — and the beneficiary has no say. The trustee still owes fiduciary duty, but the range of decisions they can make is very wide.

-

Supplemental Needs Trust (SNT)A trust designed specifically for someone with a disability. The money supplements government benefits (like Medicaid or SSI) without disqualifying the person from receiving them. The rules are strict about what the money can and can’t be used for.

-

Distribution CapA limit on how much money can be taken out of the trust per year. If the cap is 10%, and the trust holds $100,000, you can’t take out more than $10,000 in a given year — no matter what.

-

IrrevocableCan’t be changed or taken back. Once the trust is set up, the settlor can’t undo it or reclaim the assets. The rules are permanent.

-

Per StirpesA Latin phrase meaning “by branch.” If a beneficiary dies, their share goes to their children rather than being redistributed to other beneficiaries. It keeps the money flowing down a family line.

-

Spendthrift ProvisionA rule that prevents the beneficiary from pledging, selling, or giving away their future trust distributions. It also stops creditors from seizing those distributions before they’re paid out.

-

Power of AppointmentThe right to decide who gets the trust money after you die. If a trust gives you this power, you can name new beneficiaries in your will or through another legal document.

-

Bloodline TrustA trust designed to keep assets within a specific family line. If a beneficiary divorces, for example, the ex-spouse can’t claim trust assets because they were never “theirs” — they belong to the bloodline.

What Happened in This Case

Now that you know how a trust is supposed to work, here’s what it looked like when one didn’t.

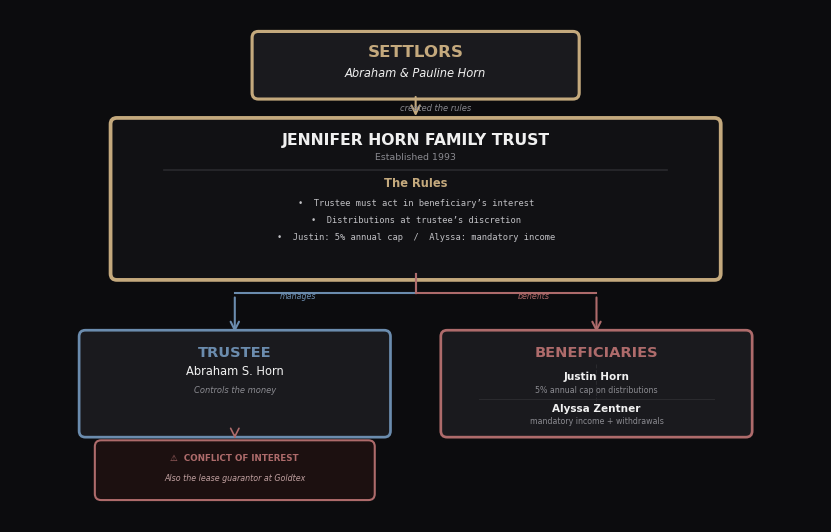

The Jennifer Horn Family Trust was created in 1993 by Abraham and Pauline Horn for their disabled daughter Jennifer. The trust was meant to protect her — to make sure she’d be taken care of for the rest of her life.

The current structure of the Jennifer Horn Family Trust, as amended March 28, 2025.

Here’s what happened over time:

- The trust is created. Both parents — Abraham and Pauline — serve as co-trustees. Two people watching the money. Two sets of eyes on every decision.

- Abraham becomes the sole acting trustee. Now one person controls everything — the rules, the money, and the decisions — with no one looking over his shoulder.

- Justin is named as a successor trustee. This means if something happens to the current trustee, Justin would step in to manage the trust.

- The rules change. Justin’s access to trust distributions is capped at 10% per year. Meanwhile, his sister Alyssa receives mandatory income distributions and withdrawal rights. Same trust, different rules for different children.

- Justin is removed as successor trustee. The person who was supposed to be next in line to manage the trust is taken out of the chain of succession entirely.

- Justin’s cap is cut in half — from 10% to 5%. The 2018 amendment is revoked, and new disability provisions are added. If Justin is classified as disabled, all of his distributions become restricted to 19 specific categories — and the trustee controls every dollar.

- The trustee sends Justin disability paperwork. Six days after signing an amendment that gives the trustee more control if Justin is disabled, the trustee asks Justin to prove he’s disabled. The sequence matters.

The trustee is also the lease guarantor for Justin’s apartment — meaning he has a personal financial interest in whether Justin stays or goes. One person holds three roles: settlor (through amendments), trustee (controlling distributions), and guarantor (financially exposed to Justin’s housing). These are roles that should never be held by one person because the conflicts between them are irreconcilable.

Red Flags in Any Trust

This section isn’t just about Justin’s case. These are warning signs that apply to any trust situation. If you recognize these patterns in your own life, pay attention.

- The trustee refuses to provide an accounting when asked. You have a right to know where the money is going. In most states, this is a legal right, not a favor. A trustee who won’t show you the books is hiding something or doesn’t want to be held accountable.

- The trustee benefits personally from decisions they make about your money. If the trustee stands to gain — financially, logistically, or otherwise — from the way they distribute trust funds, that is a conflict of interest. Fiduciary duty requires the trustee to put you first, not themselves.

- The trustee pushes you toward a classification that gives them more control. If the trust rules say the trustee gets more power over your money when you’re classified a certain way — and then the trustee actively tries to get you classified that way — the incentive structure is backwards. They’re not protecting you. They’re expanding their authority.

- Distribution rules are different for different beneficiaries without clear justification. If one sibling gets mandatory income and withdrawal rights while the other is capped at a small percentage with no say, ask why. Sometimes there are legitimate reasons. Sometimes the answer is favoritism written into law.

- The same person is both the one making rules and the one enforcing them. When the settlor and trustee are the same person — or when the trustee has the power to amend the trust — there is no check on their authority. They write the rules and then decide how to follow them.

- The trustee says things like “why should I jeopardize MY credit” when spending YOUR trust money. The moment a trustee frames their fiduciary obligation as a personal sacrifice or risk to themselves, they’ve revealed the conflict. The trust money is not their money. The risk they’re worried about is not a trust concern — it’s a personal one.

- The trustee threatens to cut you off if you don’t comply with their demands. Trust distributions are governed by the trust document, not by the trustee’s mood. A trustee who threatens to withhold money unless you do what they say is using the trust as a weapon, not a shield.

What You Can Do

If something about your trust situation feels wrong, you are not powerless. You have options, and most of them don’t require a lawyer to start.

-

1Request an accounting.

In most states, a beneficiary has the legal right to a full accounting of trust activity — every deposit, withdrawal, and investment. Put the request in writing. If the trustee refuses, that refusal itself is evidence of a problem.

-

2Consult a trust attorney.

Many trust and estate attorneys offer free initial consultations. You don’t need to file a lawsuit to get advice. Even a 30-minute conversation can tell you whether your concerns are justified and what your options are.

-

3File a complaint with your state’s probate court.

Probate courts have jurisdiction over trusts. If a trustee is violating their duties, you can petition the court to intervene — to compel an accounting, remove the trustee, or appoint a replacement.

-

4Document everything.

Save every text, email, letter, and financial record related to the trust. If the trustee says something revealing in a conversation, write it down immediately with the date and time. Documentation is the foundation of every successful legal claim.

-

5Read the trust document itself.

You have the right to a copy of the trust. Read it. You don’t need a law degree to understand most of it — and the glossary above will help with the legal terms. Knowing what the document actually says is the first step to knowing whether the trustee is following it.

Resources

New Jersey Probate Court — Self-Help Resources

Information on filing trust-related petitions in NJ courts.

The Full Report — Trust Track

The documented record of the Jennifer Horn Family Trust, with source documents and legal analysis.

The Story

The full narrative of what happened, including the trust track alongside the building and court tracks.

A trust is supposed to protect the people who need it most. When the person holding the money is also the person making the rules, rewriting them, and deciding whether you qualify for your own inheritance — that isn’t protection. It’s control. Understanding how trusts work is the first step to recognizing when one isn’t working the way it should.